As you explore mortgage options to finance your new home, you may come across the concept of a “rate buy-down.” This is a valuable strategy that allows you to secure a lower mortgage interest rate, which can lead to significant savings over the life of your loan. In this article, we’ll walk you through what a rate buy-down is, the potential benefits and challenges, and how it could apply in a real-world scenario for a $500,000 home.

What Is a Rate Buy-Down?

A rate buy-down, also known as a mortgage discount point, involves paying an upfront fee to reduce your interest rate. Essentially, you are prepaying some of the interest costs to lower your monthly mortgage payments. This process can be particularly helpful in high-interest rate environments, making homeownership more affordable over time.

Rate buy-downs are often discussed in terms of “points,” where one point equals 1% of the loan amount. Each point you purchase lowers your interest rate by a certain percentage, generally between 0.125% and 0.25% per point, though the exact rate reduction can vary depending on the lender and market conditions.

How Does It Work?

Here’s a quick breakdown:

- Determine the Loan Amount: To figure out how much you would need to pay, calculate 1% of your loan amount (not the purchase price, but the amount you’re borrowing).

- Evaluate the Rate Reduction: Each point reduces your interest rate slightly, and you can buy multiple points to bring the rate down even further.

- Consider the Cost-Benefit Ratio: Buying down the rate may not always make sense, so it’s important to calculate how much you’ll save each month and how long it will take to break even.

Example: Buying Down the Rate on a $500,000 Home

Let’s use a $500,000 home purchase as an example. If you’re planning to make a 20% down payment, you’ll be borrowing $400,000.

Suppose your lender offers you a 6% interest rate on a 30-year fixed-rate mortgage. Your monthly principal and interest payment on that loan would be approximately $2,398. If you buy one discount point (1% of $400,000, or $4,000), your lender might reduce your rate to 5.75%, lowering your monthly payment to around $2,334. This results in monthly savings of $64.

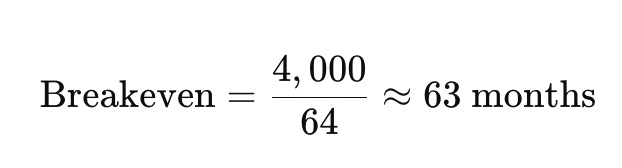

To calculate the breakeven point for buying this point, divide the upfront cost by the monthly savings:

In this scenario, it would take just over five years (63 months) to recoup the upfront cost of buying down the rate. If you plan to keep the mortgage for at least this time, buying down the rate may be worthwhile.

Benefits of Buying Down Your Rate

- Lower Monthly Payments: The most immediate benefit of a rate buy-down is reduced monthly payments. Even a small reduction in interest can save you thousands over the life of your loan.

- Increased Affordability: If high monthly payments are a concern, buying down your rate can make the mortgage more affordable, freeing up money for other expenses or savings goals.

- Long-Term Savings: By reducing your interest rate, you lower the total interest paid over the life of the loan. Even with upfront costs, the potential long-term savings can be substantial, especially for 30-year mortgages.

- Better Budgeting: Fixed-rate mortgages with bought-down rates offer predictable monthly payments, making it easier to plan your finances over the long term.

Challenges and Considerations

- Upfront Cost: The primary challenge is the upfront cost. Purchasing points requires cash at closing, which may be difficult if you’re already stretching your budget for a down payment, closing costs, and moving expenses.

- Breakeven Point: Calculating the breakeven point is essential. If you don’t plan to stay in the home long enough to reach that point, buying down the rate might not save you money in the end.

- Opportunity Cost: Using cash to buy down your rate could mean less money available for other financial goals, such as investments, emergency savings, or home improvements. Consider whether the potential savings are worth this trade-off.

- Loan Restrictions: Some types of loans, like certain adjustable-rate mortgages (ARMs), may not allow rate buy-downs or may limit their effectiveness. Make sure to discuss with your lender if this strategy is compatible with your loan product.

When Is Buying Down Your Rate a Good Idea?

A rate buy-down is often a good choice if:

- You plan to stay in the home long-term: The longer you stay, the more you save in interest over time.

- You have extra cash available: If you have enough cash to cover the upfront cost without affecting your other financial goals, buying down the rate may provide valuable long-term savings.

- You’re in a high-interest-rate environment: In times when mortgage rates are high, buying down your rate can help make homeownership more affordable.

Final Thoughts

Buying down your mortgage rate can be a powerful tool in making homeownership more affordable. However, it requires careful calculation to ensure that it aligns with your financial situation and homeownership timeline. By considering the cost, savings, and breakeven point, you can decide if a rate buy-down is right for you.

If you’re considering buying a home and want to explore rate buy-down options, be sure to discuss them with your lender. They can help you determine the best approach based on current rates, your budget, and how long you plan to stay in the home. With the right information, you can make an informed decision that leads to a more affordable and manageable mortgage.